Ignite Change

"You can't really move forward until you look back."

– Dr. Cornel West, During a discussion about persistent poverty

At VCCSE, we’re reflecting on the roots of community development finance to better understand our progress so far, and to clearly define our future role, mission, and potential impact.

Scroll down or use the quick links below to learn more.

Our Mission

The Need to Go Deeper

Our guiding principles of Partnership, Innovation, and Expertise have provided an instrumental framework over the last 15 years.

Shortly after Virginia Community Capital was founded in 2006 thanks to a $15 million state-backed seed investment under then-Governor Mark Warner, we realized these principles were key to pursuing our mission.

Through collaboration with likeminded clients, funders, and partners, a spirit of innovation that permeates the entire organization, and a dedication to increasing access to capital and resources in under-resourced communities, we’ve generated over $1.92 billion in impact in Virginia and beyond as we pursue equity in community and economic development.

While we’re very proud of the progress we’ve made together, 2021 taught us that we can and must go deeper. Guiding principles are important, but even more vital are values. This year, we’re taking a much closer look at our mission and strategic goals, and we’re challenging ourselves to fully understand the visions our communities have for themselves and the work that will best support them. In addition, we will work to ensure everyone has access to the same opportunities based on their unique needs. We recognize that advantages and barriers exist and, as a result, we don’t all start from the same place.

As we strive to make this period more than a moment, this is a time of listening, learning, and growing at Virginia Community Capital and LOCUS Impact Investing. Because movements don’t just move, they evolve – and we must evolve with them.

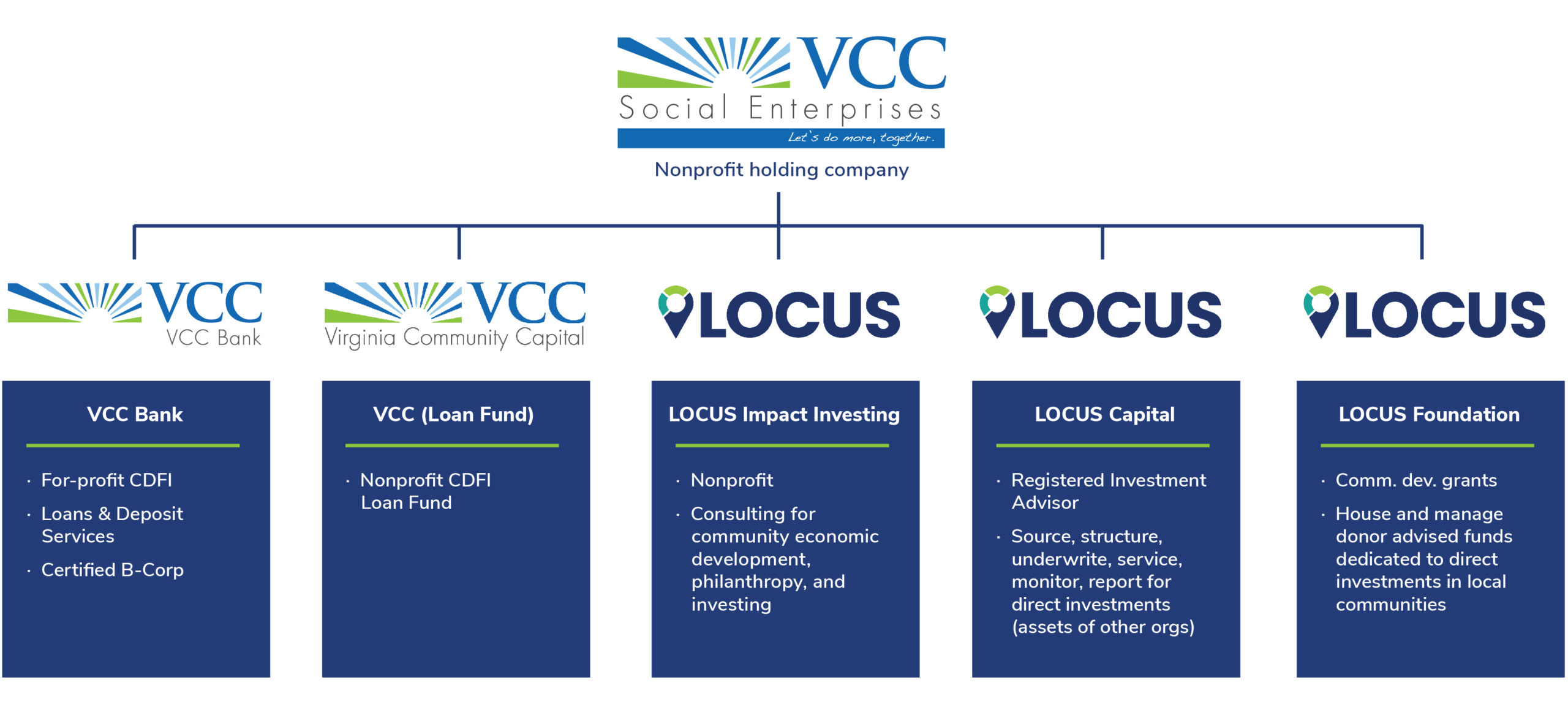

Our Structure

More Than a Bank

CDFIs can take several forms – loan funds, community banks or credit unions – but our organization is particularly unique in its structure.

Every facet of VCCSE was strategically designed with our values and commitment to positive social change in mind. Our unique products and programs were developed by identifying needs, filling gaps, and offering a suite of services that – collectively or individually – can meet almost any community development stakeholder wherever they are in their journey.

How do we work?

Our nonprofit holding company, VCC Social Enterprises, is the parent organization. VCC Bank is a for-profit CDFI bank, offering loans and deposit services, and Virginia Community Capital is our nonprofit CDFI loan fund.

LOCUS Impact Investing includes the nonprofit consultancy, the registered investment advisor (LOCUS Capital), and LOCUS Foundation, an entity that can house and manage donor advised funds and deploy community development grants.

LOCUS is also the program manager for the Community Investment Guarantee Pool (CIGP), a first-of-its-kind national financing tool for intermediaries participating in affordable housing, small business and climate lending.

Origin Story

Where It Started

The roots of community development finance were nurtured by movements that were in motion long before the CDFI Fund was developed in 1994.

In fact, the establishment of the first CDFI in the United States was in 1973, on the heels of the Civil Rights Movement of the 1950s and 1960s. This was followed by the passage of the Community Reinvestment Act (CRA) of 1977, which was enacted as a response to discriminatory lending practices – particularly redlining – and set the standard that banks must fulfill the lending needs of their communities, including those with fewer financial means (Office of the Comptroller of the Currency, 2014).

When the CDFI Fund was finally introduced, it sought to foster the development of loan funds and financial institutions that focus on the expansion of opportunities in economically excluded communities. At the time of the Fund’s launch, it was said, “For every $1 in CDFI Fund awards, CDFIs generate $12 in financing to communities and residents.”

Since then, CDFIs have been delivering on that vision. According to Opportunity Finance Network (OFN), their network of over 360 CDFIs has deployed over $34 billion in financing in the past 30 years, which translates into 2.19 million jobs created or retained, 535,000 businesses and microenterprises supported, 2.23 million housing units built, and 13,200 community facilities developed.

1,100

CDFIs To Date

The CDFI Fund has certified over 1,100 CDFIs to date, and a key element of these institutions is their accountability to the communities they serve. This history is the foundation on which we built our mission and business model 15 years ago, and we’ve strived to stay true to the original movement as we’ve grown into much more than a bank.

The CDFI Difference

How We Help

On the surface, one may not immediately recognize the difference between a community development financial institution and a regular bank. After all, they both make loans and offer traditional banking products. They are both regulated and insured by the FDIC (or the National Credit Union Administration, in the case of credit unions).

However, at closer inspection, there are some crucial differentiators for CDFIs. Our friends at CNote explain this at length on their blog, but here are key points:

- CDFIs are required to direct at least 60% of their lending capital and other resources to low-income communities.

- CDFIs offer products and programs that support high-impact projects not served by traditional finance.

- CDFIs can take on more risk due to their more flexible underwriting standards.

- CDFIs offer resources beyond capital, such as technical assistance and advisory services.

- CDFIs offer more flexibility in their loan servicing and are more willing to adjust lending terms to enable community benefit.

We think our partners at OFN put it perfectly when they said, “We see possibilities where others see risk.”

Focus Areas

Community Development

As defined by the World Health Organization (WHO), social determinants of health (SDOH) are “the conditions in which people are born, grow, work, live, and age, and the wider set of forces and systems shaping the conditions of daily life, including economic policies and systems, development agendas, social norms, social policies, and political systems.”

At VCCSE, we use SDOH as a framework for thinking about the complex intersections between our focus areas – like housing, health, and climate – as well as the role of community reinvestment in promoting equitable development in Virginia. An ever-increasing body of research demonstrates that factors such as income, jobs, housing, environment, food access, education, and neighborhood conditions exert a powerful impact on a person’s health status and life expectancy.

To encourage more conversations around SDOH, and to better address all our communities’ aspirations, we believe all actors in the community development and finance world should be asking questions that go beyond just affordable housing, just physical health, just education, and so on.

Acknowledging that all community development sectors intersect will elevate our work and lead to more holistic positive change.

Healthy People 2030, U.S. Department of Health and Human Services, Office of Disease Prevention and Health Promotion. Retrieved March 2022, from health.gov

Let’s do more, together.

There are many ways to partner with VCC Social Enterprises on the road toward equity. Are you our next visionary collaborator?